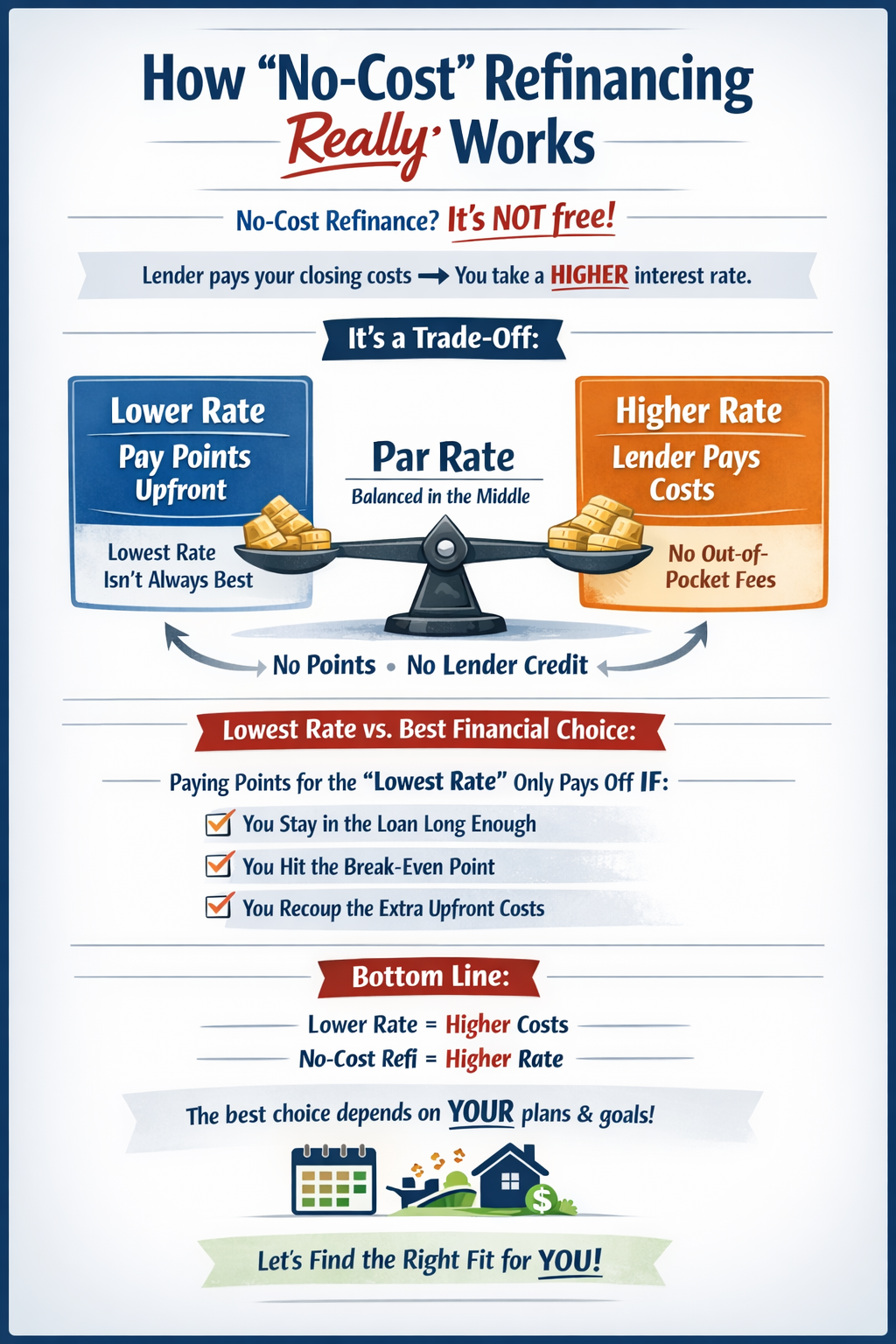

When people hear “no-cost refinance,” they usually think one thing:

“Free.”

But that’s not what it means.

A no-cost refinance simply means you’re not paying closing costs out of pocket.

Instead, those costs are covered by the lender — in exchange for a slightly higher interest rate.

First, Let’s Talk About the Trade-Off

Every refinance comes down to one simple balance:

Interest Rate ↔ Loan Costs

You can’t move one without affecting the other.

Option 1: Lower Rate

If you want the lowest possible rate, you usually have to pay points upfront.

- “Points” are prepaid interest.

- 1 point = 1% of your loan amount.

- Paying points lowers your rate.

But lowering the rate increases your upfront cost.

Option 2: No-Cost Refinance

If you don’t want to pay closing costs upfront:

- You accept a slightly higher rate.

- The lender gives you a credit.

- That credit covers your closing costs.

So the loan isn’t free — the costs are just built into the rate.

What Is the “Par Rate”?

Think of it like an old-fashioned balance scale.

The Par Rate is the neutral middle point.

At Par:

- No points are paid.

- No lender credit is received.

- The rate and costs are balanced.

This is typically where I start when quoting options — it gives us a clean, neutral baseline to compare from.

From there, we can move in either direction depending on your goals.

Why the “Lowest Rate” Isn’t Always the Smartest Choice

A lot of borrowers say:

“Just give me the lowest rate possible.”

But here’s what matters:

If you pay points to get a lower rate, you’re spending money upfront.

That only makes sense if you stay in the loan long enough to recover that cost.

This is called the Breakeven Point.

What Is a Breakeven Point?

Breakeven = How long it takes for your monthly savings to recover the upfront cost of paying points.

Example:

- You pay $4,000 in points.

- You save $150 per month.

- $4,000 ? $150 = about 27 months.

That means you must stay in that loan at least 27 months just to break even.

If you refinance, sell, or pay off the loan before that?

You never recover that $4,000.

So What’s Actually the “Best” Rate?

The best rate isn’t always the lowest rate.

The best rate is the one that fits:

- How long you plan to stay in the home

- Whether you may refinance again

- Your monthly payment goals

- Your cash flow preferences

- Your long-term financial strategy

Sometimes:

- Paying points makes sense.

- Taking Par makes sense.

- Doing a no-cost refinance makes sense.

There is no one-size-fits-all answer.

The Bottom Line

Lower Rate = Higher Upfront Cost

Higher Rate = Lower or No Upfront Cost

There’s no such thing as a free loan.

There’s only how you structure it.

The right structure depends entirely on your situation.

And that’s exactly why I walk my clients through multiple options — so you can see the numbers clearly and choose what actually benefits you long term.

The post How “No-Cost” Refinancing Really Works appeared first on Amir Salah - Senior Mortgage Loan Consultant.

]]>

Adjustable Rate Mortgages (ARMs) tie the interest rate to an external benchmark or index. The rate changes periodically based on fluctuations in this index. Commonly used indices for ARMs include:

- Secured Overnight Financing Rate (SOFR): A relatively new index that has replaced the LIBOR in many loans.

- Constant Maturity Treasury (CMT): Based on U.S. Treasury yields.

- Cost of Funds Index (COFI): Reflects the cost of savings institutions obtaining funds.

The interest rate on the ARM is typically composed of two parts:

- Index Rate: The fluctuating rate tied to the chosen benchmark.

- Margin: A fixed percentage added to the index rate by the lender, which remains constant.

For example, if your ARM is tied to SOFR, and the SOFR rate is 2%, and the margin is 2.5%, your interest rate would be 4.5% at that adjustment period.

What does a 10/6 MONTH SOFR ARM mean and how does it work?

A 10/6 month SOFR ARM is a type of adjustable-rate mortgage where the interest rate is fixed for the first 10 years, and after that, it adjusts every 6 months based on the SOFR (Secured Overnight Financing Rate) index. Here’s how it works:

Breaking Down the Terms:

- 10: The interest rate is fixed for the first 10 years. During this period, the borrower enjoys a stable, predictable monthly payment.

- 6 months: After the initial 10-year fixed period, the rate adjusts every 6 months. The adjustment is based on the SOFR index plus a margin set by the lender.

- SOFR (Secured Overnight Financing Rate): This is the index that the interest rate is tied to. SOFR reflects the cost of borrowing cash overnight, which is often considered a more reliable and transparent benchmark than the older LIBOR index.

How It Works:

- Initial Period (10 Years Fixed): For the first 10 years, the interest rate remains constant, and your payments are predictable.

- Adjustment Period (After 10 Years): Once the 10-year fixed period ends, the rate adjusts every 6 months according to the current SOFR index rate at that time. The rate for each 6-month period is calculated by adding a predetermined margin (which could be something like 2% or 2.5%) to the current SOFR rate.

For example, if the SOFR at the time of adjustment is 1.5% and the margin is 2%, the new interest rate for the next 6 months would be 3.5%.

- Caps and Limits: Most ARMs, including SOFR ARMs, have interest rate caps to protect borrowers from extreme increases. There are typically:

- Initial adjustment cap: Limits how much the rate can increase during the first adjustment after the fixed period.

- Subsequent adjustment cap: Limits how much the rate can increase in each subsequent adjustment.

- Lifetime cap: Limits the maximum increase over the life of the loan.

Example:

If you start with a 10/6 SOFR ARM at an initial rate of 3.5%, it remains 3.5% for the first 10 years. After that, if SOFR rises to 2% and your margin is 2.5%, your rate would adjust to 4.5% for the next 6 months. Every 6 months, the rate could go up or down depending on the SOFR rate at that time.

Key Points to Consider:

- Predictability: You have 10 years of a stable rate, which can be helpful if you plan to sell or refinance within that time.

- Potential Risk: After 10 years, the rate could rise significantly depending on the movement of SOFR.

- Rate Caps: These help protect against extreme rate increases but still allow for adjustments every 6 months.

Why would someone get an ARM as opposed to a Fixed?

There are several reasons why someone might choose an Adjustable Rate Mortgage (ARM) over a Fixed-Rate Mortgage, depending on their financial situation, future plans, and risk tolerance. Here are the key factors:

-

Lower Initial Interest Rates

- Benefit: ARMs typically offer lower interest rates during the initial fixed period (e.g., the first 5, 7, or 10 years) compared to fixed-rate mortgages.

- Why it matters: A lower initial rate can result in significantly lower monthly payments at the beginning of the loan, which may appeal to borrowers looking to maximize cash flow in the short term.

-

Short-Term Homeownership

- Benefit: If a borrower plans to sell the home or refinance before the ARM starts adjusting (e.g., within the first 5, 7, or 10 years), they can take advantage of the lower interest rate without ever experiencing the adjustment period.

- Why it matters: For people who expect to move, sell, or refinance in the short term, the lower initial rate of an ARM can save them money without exposing them to the risk of future rate hikes.

-

Higher Affordability

- Benefit: The lower initial payments may help borrowers afford a more expensive home or qualify for a larger loan than they would with a fixed-rate mortgage.

- Why it matters: In a competitive housing market, ARMs can make homes more affordable in the short term, enabling buyers to purchase in higher-priced areas or more desirable neighborhoods.

-

Expectation of Falling Interest Rates

- Benefit: If interest rates are expected to drop in the future, some borrowers may opt for an ARM, anticipating that their rate will adjust downward once the fixed period ends.

- Why it matters: If rates decline, the borrower could enjoy lower payments after the adjustment period, while those with fixed-rate mortgages would need to refinance to benefit from the lower rates.

-

Short-Term Financial Strategy

- Benefit: Borrowers who have other short-term financial goals, such as paying off other debts or investing the savings from lower mortgage payments, may prefer an ARM.

- Why it matters: The savings from the lower initial rate can be redirected toward other financial priorities, such as building an emergency fund, investing, or paying down high-interest debt.

-

Inflation and Income Growth

- Benefit: For those expecting their income to grow in the future, an ARM may be less risky, as they will be better equipped to handle potential payment increases when the rate adjusts.

- Why it matters: Borrowers confident in future salary increases may not be as concerned about higher payments after the initial period.

Potential Drawbacks of ARMs (Compared to Fixed Rates)

- Uncertainty: After the initial fixed period, the rate and payment amount can increase, making ARMs less predictable than fixed-rate mortgages.

- Risk of Rate Increases: If interest rates rise significantly, borrowers could face much higher monthly payments after the adjustment period, leading to financial stress.

- Complexity: ARMs can have various adjustment schedules, caps, and terms that may be confusing for some borrowers, requiring a deeper understanding of how the loan works.

Who Might Prefer a Fixed-Rate Mortgage?

- Long-Term Stability: People who plan to stay in their home for many years (10+ years) may prefer the predictability of a fixed-rate mortgage, which locks in the same payment throughout the life of the loan.

- Risk-Averse Borrowers: Those who prefer stability and don’t want to worry about rising interest rates and fluctuating payments will likely lean toward a fixed-rate loan.

Summary of Pros and Cons:

| ARM (Adjustable Rate Mortgage) | Fixed-Rate Mortgage |

| Lower initial interest rate | Stable, predictable payments |

| Good for short-term homeownership | Good for long-term homeownership |

| Rate adjusts based on the market | Locked rate for entire term |

| Potential for rising rates | No risk of rate increase |

| More affordable in the short term | Higher initial interest rate |

Ultimately, someone might choose an ARM if they want lower initial payments, plan to sell or refinance within the fixed period, or are willing to take the risk that rates could go up. Conversely, fixed-rate mortgages are better suited for borrowers seeking long-term stability and predictability.

The post What do Adjustable Rate Mortgages tie the rate to? appeared first on Amir Salah - Senior Mortgage Loan Consultant.

]]>

What Is Debt-to-Income (DTI) Ratio in Mortgage Lending?

If you’re planning to buy a home or refinance your mortgage, one of the most important numbers you’ll hear about is your Debt-to-Income Ratio, or DTI. It’s a key part of mortgage lending and understanding it can help you prepare and potentially qualify for better loan options.

Definition of DTI

The Debt-to-Income (DTI) ratio is a financial metric that compares how much you owe each month to how much you earn. Lenders use it to assess your ability to repay a mortgage.

It’s calculated using the following formula:

DTI Ratio = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

This gives you a percentage that helps lenders understand your financial balance between income and obligations.

Two Types of DTI Ratios

Mortgage lenders typically look at two versions of your DTI:

1. Front-End Ratio (Housing Ratio)

- Focuses only on housing-related costs:

- Mortgage principal & interest

- Property taxes

- Homeowners insurance

- HOA dues (if any)

- Formula: Housing Costs ÷ Gross Monthly Income

2. Back-End Ratio

- Includes all monthly debt obligations, such as:

- Housing costs

- Credit cards

- Car loans

- Student loans

- Personal loans

- Alimony/child support

- Formula: Total Monthly Debts ÷ Gross Monthly Income

Most lenders care more about the back-end ratio, but both can play a role in mortgage approval.

Example Scenarios

Let’s look at two real-life examples to make this easier to understand:

Example 1: High Income, High Debt

- Gross Monthly Income: $15,000

- Total Monthly Debts: $7,000 (mortgage, car, student loans, credit cards)

- DTI = (7,000 ÷ 15,000) × 100 = 46.67%

Even though the income is high, the high debt leads to a DTI of 46.67%, which could limit mortgage options under stricter programs.

Example 2: Moderate Income, Low Debt

- Gross Monthly Income: $6,000

- Total Monthly Debts: $600 (car loan and small credit card balances)

- DTI = (600 ÷ 6,000) × 100 = 10%

This person has a low DTI and could qualify for a larger mortgage despite having a more modest income.

What’s a Good DTI Ratio?

Generally speaking:

- Below 36% = Strong and favorable

- 37%–43% = Acceptable, depending on the loan program

- 44%+ = May need compensating factors (high credit score, assets, etc.)

DTI Requirements by Loan Type

Different loans have different DTI limits. Here’s a quick breakdown:

Conventional Loans (Fannie Mae/Freddie Mac):

- Preferred: 36% or less

- Max: Up to 45% (sometimes 50% with strong credit and reserves)

FHA Loans:

- More lenient

- Back-end DTI allowed up to 50–56.9% in some cases

VA Loans (for Veterans and Active Military):

- Benchmark: 41%

- Flexible with strong residual income (money left after monthly expenses)

Jumbo Loans:

- Used for high-value properties

- Typically capped at 43% or lower

HELOCs (Home Equity Line of Credit):

- DTI usually capped around 43%–45%, but varies by lender

Additional Considerations

- Different income types: Bonuses, commissions, or self-employment income may require extra documentation or a 2-year average.

- Not all debts count: Debts with fewer than 10 months left may be excluded, depending on the loan program.

- Higher DTI = higher risk: Lenders may offer smaller loan amounts or higher rates.

- Lower DTI = stronger borrower: More likely to be approved and qualify for better terms.

Why DTI Matters

Understanding your DTI helps you:

- Know how much home you can afford

- Strategize debt reduction before applying

- Select the best loan program for your situation

Need Help Calculating Your DTI?

If you’re unsure where you stand, don’t worry—I can help break down your numbers and see what loan options might be a good fit. Whether you’re looking to buy your first home, refinance, or tap into your home equity, your DTI is a great place to start.

Let’s chat!

The post Debt to Income Ratio aka DTI Explained appeared first on Amir Salah - Senior Mortgage Loan Consultant.

]]>

“How the NAR Settlement Empowers Homebuyers: Key Changes to Know Before August 17th”

The recent settlement between the National Association of Realtors® (NAR) and various plaintiffs is set to introduce significant changes to the real estate industry. These changes, aimed at increasing transparency and fairness, will officially take effect on August 17, 2024. As a homebuyer, it’s essential to understand how these updates will impact your journey to homeownership. Here’s a breakdown of the key changes and what they mean for you.

Written Agreements Before Home Tours

One of the most notable changes is the requirement for written agreements between buyers and their agents before any property tours take place. This change ensures that both parties have a clear understanding of the services being provided and the fees involved from the very beginning. For you, this means fewer surprises and a more transparent relationship with your agent. You’ll know exactly what services you are receiving and how much they will cost before you even step foot inside a home.

Compensation Disclosure: Transparency in Agent Earnings

Under the new rules, real estate agents must provide a detailed breakdown of their compensation. This means that as a buyer, you will have full visibility into how much your agent is earning from your transaction, whether it’s through a portion of the seller’s commission, a fixed fee, or another method. This increased transparency allows you to make more informed decisions about your finances and ensures that you understand where your money is going.

Negotiable Commissions: Flexibility in Fees

Another critical aspect of the settlement is the emphasis on the negotiability of real estate commissions. Despite common misconceptions, commission rates are not set in stone and can vary significantly. The new rules reinforce that you, as a buyer, have the right to negotiate these fees with your agent. This flexibility allows you to find an arrangement that best suits your financial situation and ensures that you are getting value for your money.

What Does This Mean for You?

While these changes may seem daunting, they are ultimately designed to benefit you, the homebuyer. By increasing transparency and ensuring clear communication between you and your agent, the NAR settlement aims to make the homebuying process fairer and more straightforward. As these new rules take effect on August 17, 2024, it’s important to stay informed and be proactive in understanding how they impact your homebuying experience.

For more detailed information on these changes and how they might affect you, feel free to read the full article on NAR’s website.

If you have any questions or need further clarification, don’t hesitate to reach out. Your journey to homeownership should be as smooth and transparent as possible, and these changes are a step in that direction.

The post Understanding the NAR Settlement: What Homebuyers Need to Know appeared first on Amir Salah - Senior Mortgage Loan Consultant.

]]>

The National Association of Realtors® (NAR) is set to implement significant changes on August 17, 2024, as part of a settlement agreement designed to address claims related to broker commissions. These changes, aimed at increasing transparency and fairness in real estate transactions, will affect MLS policies and practices across the country.

Key Changes Effective August 17, 2024

- Elimination of Mandatory Compensation Offers: One of the most impactful changes is the removal of any requirement to offer compensation to buyer brokers or other buyer representatives through the MLS. This means that while compensation can still be offered, it will no longer be a default or mandatory practice within the MLS. Listing brokers and sellers can still decide to offer compensation, but this will now occur outside the MLS framework.

- Redefining Cooperation: The concept of cooperation within the MLS is also being redefined. The new policy emphasizes the sharing of property information and making properties available for showings based on what is in the best interest of clients, rather than tied to compensation.

- Disclosure Requirements: MLS participants working with buyers must now enter into a written agreement with the buyer before showing properties. This ensures that all parties understand the terms of their working relationship from the outset.

- Restrictions on MLS Data Usage: MLSs will be prohibited from using their data to support any platform that facilitates the offering of compensation. This aims to prevent any indirect methods of reintroducing compensation offers through alternative means.

What This Means for Realtors® in California

For many Realtors® in California, these changes might seem substantial, but the practical impact could be less dramatic. The state’s competitive and diverse real estate market has already adapted to a wide variety of practices and compensation models. Realtors® who have built strong relationships with their clients and who emphasize transparency and negotiation are likely to find that these changes merely formalize practices that are already in place.

The transition may require some adjustments, particularly in how compensation is discussed and agreed upon, but for most, it will quickly become the new normal. The focus on written agreements and clear communication should ultimately lead to more informed clients and smoother transactions, which is beneficial for all parties involved.

In conclusion, while the NAR lawsuit has prompted these significant changes, the overall impact on day-to-day operations for many California Realtors® may be minimal. It’s more about adjusting to new formalities rather than a complete overhaul of the way business is done. As with any change, there will be a period of adaptation, but this will soon become the standard practice moving forward.

For further details on these changes, you can visit the official NAR website or consult the specific FAQs and practice change summaries they have provided (www.nar.realtor)

The post Navigating the August 17th NAR Changes: What Realtors® Need to Know appeared first on Amir Salah - Senior Mortgage Loan Consultant.

]]>

In America today, consumer debt has reached an all-time high, leaving many homeowners struggling to make ends meet. The good news is, there are several options available to help consolidate and manage this debt. As a trusted mortgage professional with E Mortgage Capital, Amir Salah is dedicated to helping homeowners in California find a way out of debt.

Understanding the Consumer Debt Crisis

Consumer debt in America includes credit card debt, student loans, and personal loans, among others. Many Americans find themselves overwhelmed by these debts, struggling to keep up with payments and falling behind on other financial obligations. The current crisis has been exacerbated by the economic impact of the COVID-19 pandemic, leaving even more people in need of assistance.

Consolidation Options

For homeowners in California looking to consolidate their debt, there are several options to consider:

- Closed-End Second Mortgage: A closed-end second mortgage, also known as a home equity loan, allows homeowners to borrow against the equity in their home. This can be a good option for consolidating high-interest debt into a single, lower-interest loan.

- HELOC: A Home Equity Line of Credit (HELOC) is another way to borrow against the equity in your home. With a HELOC, you can borrow up to a certain amount, but only pay interest on the amount you actually borrow. This can be a flexible and cost-effective way to consolidate debt.

- Cash-Out Refinance: A cash-out refinance involves refinancing your existing mortgage for a higher amount than you currently owe and taking the difference in cash. This can be a good option if you have built up equity in your home and can qualify for a lower interest rate than you are currently paying on your mortgage.

Understanding Your Blended Rate

When consolidating debt, it’s important to understand the concept of the blended rate. This is the average interest rate you will pay on your consolidated debt. While your individual interest rates may increase, the overall savings from consolidating your debt could be significant. It’s important to carefully consider the long-term savings versus the short-term increase in rates.

Amir Salah and E Mortgage Capital are here to help homeowners in California navigate the consumer debt crisis. With a range of options available, including closed-end second mortgages, HELOCs, and cash-out refinancing, they can help you find the right solution for your financial situation. Don’t let debt hold you back any longer – contact Amir Salah today to learn more about how you can consolidate and manage your debt.

The post Navigating Debt: Expert Advice Homeowners appeared first on Amir Salah - Senior Mortgage Loan Consultant.

]]>The post Welcome appeared first on Amir Salah - Senior Mortgage Loan Consultant.

]]>