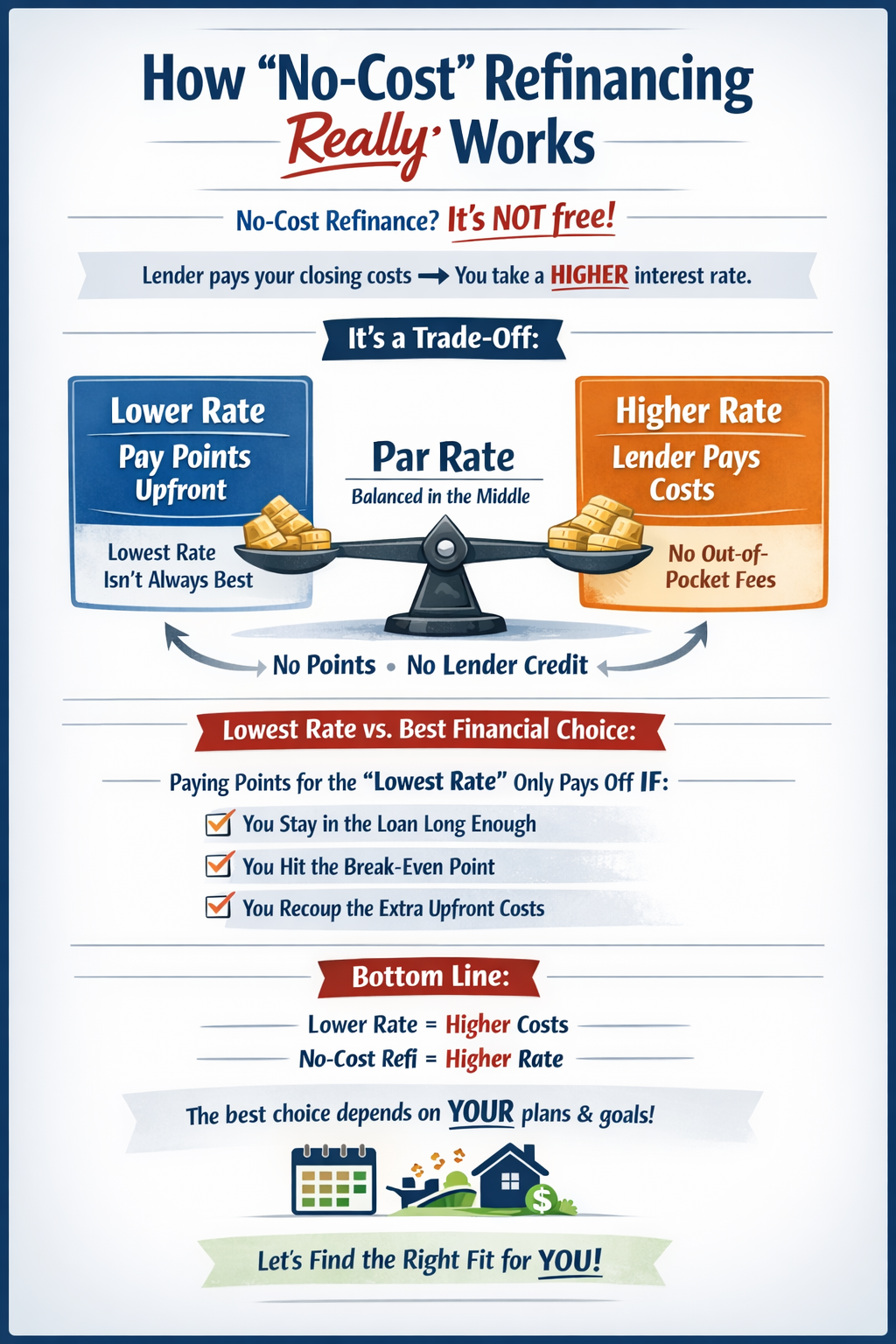

How “No-Cost” Refinancing Really Works

When people hear “no-cost refinance,” they usually think one thing:

“Free.”

But that’s not what it means.

A no-cost refinance simply means you’re not paying closing costs out of pocket.

Instead, those costs are covered by the lender — in exchange for a slightly higher interest rate.

First, Let’s Talk About the Trade-Off

Every refinance comes down to one simple balance:

Interest Rate ↔ Loan Costs

You can’t move one without affecting the other.

Option 1: Lower Rate

If you want the lowest possible rate, you usually have to pay points upfront.

- “Points” are prepaid interest.

- 1 point = 1% of your loan amount.

- Paying points lowers your rate.

But lowering the rate increases your upfront cost.

Option 2: No-Cost Refinance

If you don’t want to pay closing costs upfront:

- You accept a slightly higher rate.

- The lender gives you a credit.

- That credit covers your closing costs.

So the loan isn’t free — the costs are just built into the rate.

What Is the “Par Rate”?

Think of it like an old-fashioned balance scale.

The Par Rate is the neutral middle point.

At Par:

- No points are paid.

- No lender credit is received.

- The rate and costs are balanced.

This is typically where I start when quoting options — it gives us a clean, neutral baseline to compare from.

From there, we can move in either direction depending on your goals.

Why the “Lowest Rate” Isn’t Always the Smartest Choice

A lot of borrowers say:

“Just give me the lowest rate possible.”

But here’s what matters:

If you pay points to get a lower rate, you’re spending money upfront.

That only makes sense if you stay in the loan long enough to recover that cost.

This is called the Breakeven Point.

What Is a Breakeven Point?

Breakeven = How long it takes for your monthly savings to recover the upfront cost of paying points.

Example:

- You pay $4,000 in points.

- You save $150 per month.

- $4,000 ? $150 = about 27 months.

That means you must stay in that loan at least 27 months just to break even.

If you refinance, sell, or pay off the loan before that?

You never recover that $4,000.

So What’s Actually the “Best” Rate?

The best rate isn’t always the lowest rate.

The best rate is the one that fits:

- How long you plan to stay in the home

- Whether you may refinance again

- Your monthly payment goals

- Your cash flow preferences

- Your long-term financial strategy

Sometimes:

- Paying points makes sense.

- Taking Par makes sense.

- Doing a no-cost refinance makes sense.

There is no one-size-fits-all answer.

The Bottom Line

Lower Rate = Higher Upfront Cost

Higher Rate = Lower or No Upfront Cost

There’s no such thing as a free loan.

There’s only how you structure it.

The right structure depends entirely on your situation.

And that’s exactly why I walk my clients through multiple options — so you can see the numbers clearly and choose what actually benefits you long term.